From Oil to Inequality: Iraq’s Resource Allocation and Its Role in Economic Disparities and Import Dependence

Mahmood Baban

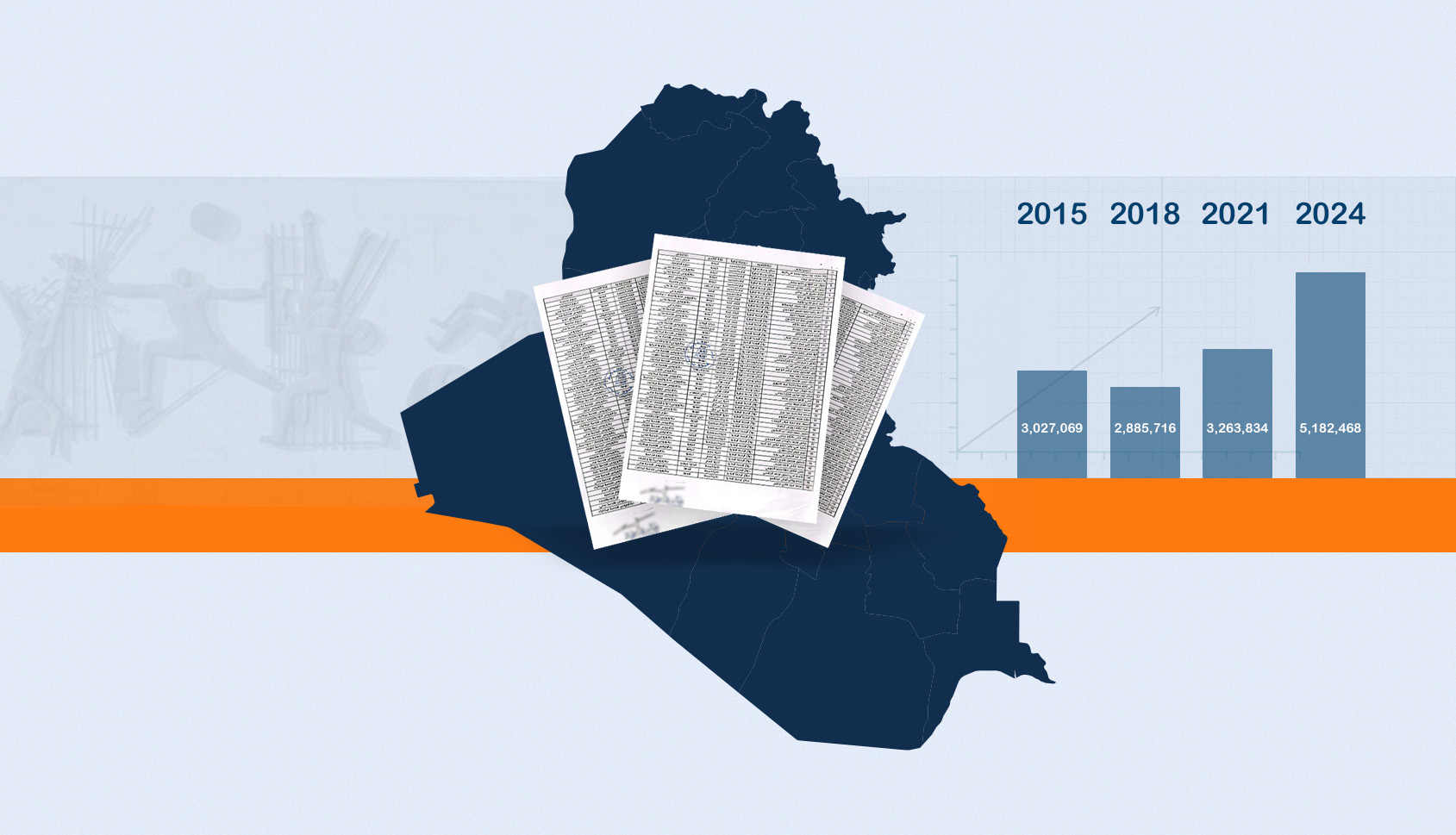

According to the Global Inequality Dashboard, which compiles data from 110 countries worldwide, Iraq ranks among the most unequal nations in terms of income and wealth distribution. The top 1% of the population earns three times more than the 45%, highlighting deep structural imbalances. A key driver of this inequality is the public sector, particularly in the way salaries are allocated.